Summary Report

Fiscal Boom

(1 votes, average: 5.00 out of 5)

(1 votes, average: 5.00 out of 5)You need to be a registered member to rate this.

Fiscal Boom

March Cut Less Likely, Inflation as a Fiscal Limit, Unwinding Financial Repression, Retailer Disruption, Equal Weight S&P Relative Value

Return of the Insidious Bear Steepener

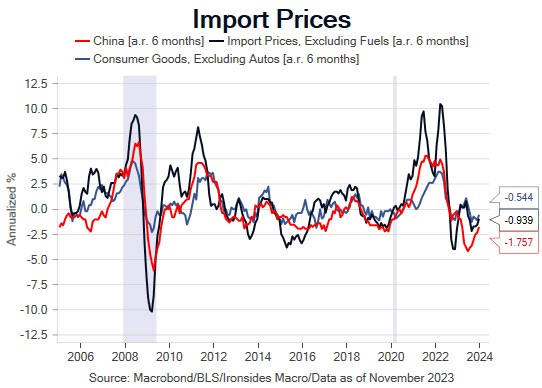

Since the December FOMC ‘pivot party’ rally, incoming data is best characterized as uncooperative for our four fours yield curve disinversion thesis. The first week of January ended with above consensus December nonfarm payrolls, a decline in the unemployment rate to 3.7% and a second consecutive 0.4% monthly increase in average hourly earnings. The second week brought a hotter than expected December CPI. This week delivered a strong December Retail Sales report for the most important month of the year for retailers. The Fed’s Beige Book was filled with qualitative evidence that demand for labor is softening, unfortunately the FOMC participant’s general view that labor supply is improving was an accurate assessment during 1H23 when prime age participation increased from 82.5% to 83.5%, however, in 2H23 it eased to 83.2%. Additionally, the layoffs & discharge rate of 1.0% is below last cycle’s low, the 1.2% insured unemployment is 0.1% above last cycle’s low and weekly initial jobless claims are showing no evidence of excess supply of labor. The evidence that labor demand is softening is convincing, if not compellingly obvious. But it is increasingly apparent, with the stall in wage disinflation the most compelling data, that the recovery of the supply of labor also stalled, thereby pushing us further from the 4% unemployment rate and 4% wage growth necessary for the FOMC to reduce the policy rate to 4% and keep the 1-year Treasury rate near 4%. Until and unless the labor market data begins to cooperate, the 49% market implied probability of a March rate cut is too high and the latest round of FOMC participant speeches prior to the quiet period ahead of the January 30-31 meeting suggested March is a stretch. There are three releases with the potential to soften Chairman Powell’s tone in the press conference: the 3Q23 advanced GDP estimate on the 25th, the December personal consumption deflator report on the 26th and 4Q23 employment cost index on the second day of the meeting.

With the return of bear steepening early in the week until the ‘final word’ from FOMC participants prior to the quiet period battered 2s, equities are behaving like much of 2023, at least until the Treasury Department’s October Quarterly Refunding Announcement and FOMC communicated an end to the rate hike cycle. Tech and related sectors are leading, with small caps and regional banks lagging. Bank earnings, with 14 of the 15 S&P components having reported, are tracking -11.2% on +1.2% revenue growth even with a 10.1% earnings surprise rate. The deeply inverted yield curve and ongoing battle over Vice Chair for Supervision, FDIC, OCC and NEC Director Brainard’s increased capital proposal are likely to pressure earnings and preclude any return of capital to shareholders. In short, banks have a profitability issue, not necessarily a liquidity or solvency problem, as was the case with US banks from 2014-2018 following the post-crisis regulatory ‘reform’ and European banks in following the sovereign debt crisis. To get to the ‘healthy broadening out’ likely requires a deterioration in the labor supply and demand imbalance that starts the rate cut cycle. Until that point, we expect a low velocity bear steepening of the Treasury curve and underperformance of financials and small caps. The selloff in the Treasury market is not yet deep enough to drag the tech sector lower, particularly given that better than expected labor market and consumption data is an integral part of the story. Keep an eye out for discussion of the Fed’s balance sheet at the press conference, post meeting speeches and minutes. We detailed our outlook for an eventual return to a ‘bills’ only policy that would reduce longer maturity rate suppression in last week’s note, Ripping off the Band-Aid.

Barry C. Knapp

Macro Strategist - Ironsides Macroeconomic

Vail, USA

Disclaimer

DISCLAIMER: Este Relatório de Análise foi elaborado e distribuído pelo Analista, signatário unicamente para uso do destinatário original, de acordo com todas as exigências previstas na Resolução CVM nº 20 de 26 de fevereiro de 2021 e tem como objetivo fornecer informações que possam auxiliar o investidor a tomar sua própria decisão de investimento, não constituindo qualquer tipo de oferta ou solicitação de compra e/ou venda de qualquer produto. As decisões de investimentos e estratégias financeiras devem ser realizadas pelo próprio leitor, os Analistas, ou a OHMRESEARCH não se responsabilizam por elas. Os produtos apresentados neste relatório podem não ser adequados para todos os tipos de investidores. Antes de qualquer decisão de investimentos, os investidores deverão realizar o processo de suitability no agente de distribuição de sua confiança e confirmar se os produtos apresentados são indicados para o seu perfil de investidor. A rentabilidade de produtos financeiros pode apresentar variações e seu preço ou valor pode aumentar ou diminuir num curto espaço de tempo. Os desempenhos anteriores não são necessariamente indicativos de resultados futuros. A rentabilidade divulgada não é líquida de impostos. As informações presentes neste material são baseadas em simulações e os resultados reais poderão ser significativamente diferentes.

O(s) signatário(s) deste relatório declara(m) que as recomendações refletem única e exclusivamente suas análises e opiniões pessoais, que foram produzidas de forma totalmente independente e que a OHMRESEARCH não tem qualquer gerência sobre este conteúdo. As opiniões aqui expressas estão sujeitas a modificações sem aviso prévio em decorrência de alterações nas condições de mercado. O Analista responsável pelo conteúdo deste relatório e pelo cumprimento da Resolução CVM nº 20/21 está indicado acima, sendo que, caso constem a indicação de mais um analista no relatório, o responsável será o primeiro analista credenciado a ser mencionado no relatório. Os analistas cadastrados na OHMRESEARCH estão obrigados ao cumprimento de todas as regras previstas no Código de Conduta da APIMEC para o Analista de Valores Mobiliários e no Manual de Controles Internos para Elaboração e Publicação de Relatórios da OHMRESEARCH. De acordo com o art. 21 da Resolução CVM nº 20/21 caso o Analista esteja em situação que possa afetar a imparcialidade do relatório ou que configure ou possa configurar conflito de interesse, este fato deverá estar explicitado no campo “Conflitos de Interesse” deste relatório.

O conteúdo deste relatório é de propriedade única do Analista signatário e não pode ser copiado, reproduzido ou distribuído, no todo ou em parte, a terceiros, sem prévia e expressa autorização deste Analista. Todas as informações utilizadas neste documento foram redigidas com base em informações públicas, de fontes consideradas fidedignas. Embora tenham sido tomadas todas as medidas razoáveis para assegurar que as informações aqui contidas não são incertas ou equívocas no momento de sua publicação, o Analista não responde pela veracidade das informações do conteúdo.

Para maiores informações, pode-se ler a Resolução CVM nº 20/21 e o Código de Conduta da APIMEC para o Analista de Valores Mobiliários. Este relatório é destinado exclusivamente ao assinante da OHMRESEARCH que o contratou. A sua reprodução ou distribuição não autorizada, sob qualquer forma, no todo ou em parte, implicará em sanções cíveis e criminais cabíveis, incluindo a obrigação de reparação de todas as perdas e danos causados, nos termos da Lei nº 9.610/98 e de outras aplicáveis.