Summary Report

Expectations Convergence

(1 votes, average: 5.00 out of 5)

(1 votes, average: 5.00 out of 5)You need to be a registered member to rate this.

Expectations Convergence

Convergence of Policy Path Expectations, Bills Only Policy, Narrower Disinflation, The Phillips Curve Comeback

The January Effect

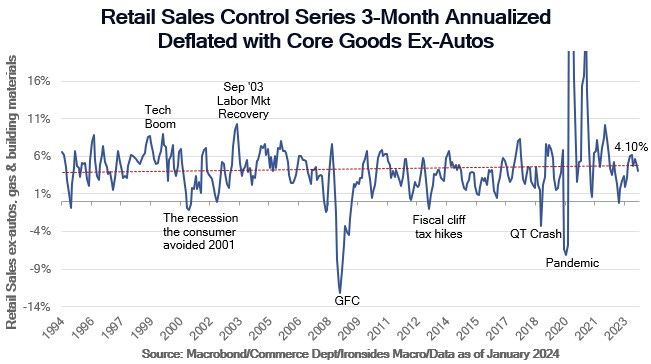

The last three January employment and CPI reports have been hotter than expected, and like the recurring pattern of soft 3Q and stronger 4Q employment growth following the Lehman bankruptcy, we suspect the pandemic-distorted seasonal adjustment factors are overstating the strength in the labor market and inflation data. That said, the sustainable broadening disinflation FOMC participant narrative and our quadrilemma (4% unemployment plus 4% wage growth facilitating a year-end ‘24 4% policy rate and 4% 10-year Treasury) were dealt a significant setback by the January employment and CPI reports, distortions or not. We will dig into the details of this week’s inflation reports later in the report, but in short, the 2H23 disinflation is highly concentrated in core goods prices that appear to be bottoming, and non-housing services inflation in the CPI and PPI reports reaccelerated in 2H23 amidst a setback in the recovery in the supply of labor. We expect cooler data in the coming months, but with the manufacturing and residential real estate sectors looking increasingly likely to expand in ‘24, and no signs of consumption weakening despite the January retail sales undershooting consensus, the hurdle for the FOMC beginning to reverse the policy tightening increased over the last couple of weeks.

A year ago, the Fed had slowed the pace of hikes from 75bp to 25bp, until the January data led the Chair to suggest in his early March Monetary Report to Congress, the FOMC might need to reaccelerate the pace to 50bp hikes. That suggestion caused a spike in real rates (TIPS yields) that exacerbated the Silicon Valley Bank run on uninsured deposits. The equity and fixed income market’s quick stabilization following the setback in the sustainable broadening of disinflation this week is a function of the convergence of the Fed and market expectations for the ‘24 policy rate path. In other words, investors took comfort that the FOMC wasn’t surprised, but what market and FOMC participants are missing is the implication of sticky services inflation for the terminal policy rate. If the FOMC only gets to 4% by the end of 2025, an increasingly likely outcome we discussed in last week’s note, The Wrong Price, pressure on banks, small businesses, real estate and federal finances will intensify. In short, 4.25% 10-year nominal Treasuries and 10-Year TIPS at 1.90%, with a -6bp term premium, are — in the words of Lee Cooperman — ‘returnless risk’ if the ‘24 year-end is likely to be 4.75% or higher. Additionally, the bounce in small caps and regional banks post-CPI is also misguided; as we discussed last week, the 200bp hit to bank return on common equity to the 10% threshold where banks build or burn capital, requires yield curve disinversion and a scrapping of the regulatory capital increase proposal to make a ‘healthy broadening’ sustainable.

Barry C. Knapp

Macro Strategist - Ironsides Macroeconomic

Vail, USA

Disclaimer

DISCLAIMER: Este Relatório de Análise foi elaborado e distribuído pelo Analista, signatário unicamente para uso do destinatário original, de acordo com todas as exigências previstas na Resolução CVM nº 20 de 26 de fevereiro de 2021 e tem como objetivo fornecer informações que possam auxiliar o investidor a tomar sua própria decisão de investimento, não constituindo qualquer tipo de oferta ou solicitação de compra e/ou venda de qualquer produto. As decisões de investimentos e estratégias financeiras devem ser realizadas pelo próprio leitor, os Analistas, ou a OHMRESEARCH não se responsabilizam por elas. Os produtos apresentados neste relatório podem não ser adequados para todos os tipos de investidores. Antes de qualquer decisão de investimentos, os investidores deverão realizar o processo de suitability no agente de distribuição de sua confiança e confirmar se os produtos apresentados são indicados para o seu perfil de investidor. A rentabilidade de produtos financeiros pode apresentar variações e seu preço ou valor pode aumentar ou diminuir num curto espaço de tempo. Os desempenhos anteriores não são necessariamente indicativos de resultados futuros. A rentabilidade divulgada não é líquida de impostos. As informações presentes neste material são baseadas em simulações e os resultados reais poderão ser significativamente diferentes.

O(s) signatário(s) deste relatório declara(m) que as recomendações refletem única e exclusivamente suas análises e opiniões pessoais, que foram produzidas de forma totalmente independente e que a OHMRESEARCH não tem qualquer gerência sobre este conteúdo. As opiniões aqui expressas estão sujeitas a modificações sem aviso prévio em decorrência de alterações nas condições de mercado. O Analista responsável pelo conteúdo deste relatório e pelo cumprimento da Resolução CVM nº 20/21 está indicado acima, sendo que, caso constem a indicação de mais um analista no relatório, o responsável será o primeiro analista credenciado a ser mencionado no relatório. Os analistas cadastrados na OHMRESEARCH estão obrigados ao cumprimento de todas as regras previstas no Código de Conduta da APIMEC para o Analista de Valores Mobiliários e no Manual de Controles Internos para Elaboração e Publicação de Relatórios da OHMRESEARCH. De acordo com o art. 21 da Resolução CVM nº 20/21 caso o Analista esteja em situação que possa afetar a imparcialidade do relatório ou que configure ou possa configurar conflito de interesse, este fato deverá estar explicitado no campo “Conflitos de Interesse” deste relatório.

O conteúdo deste relatório é de propriedade única do Analista signatário e não pode ser copiado, reproduzido ou distribuído, no todo ou em parte, a terceiros, sem prévia e expressa autorização deste Analista. Todas as informações utilizadas neste documento foram redigidas com base em informações públicas, de fontes consideradas fidedignas. Embora tenham sido tomadas todas as medidas razoáveis para assegurar que as informações aqui contidas não são incertas ou equívocas no momento de sua publicação, o Analista não responde pela veracidade das informações do conteúdo.

Para maiores informações, pode-se ler a Resolução CVM nº 20/21 e o Código de Conduta da APIMEC para o Analista de Valores Mobiliários. Este relatório é destinado exclusivamente ao assinante da OHMRESEARCH que o contratou. A sua reprodução ou distribuição não autorizada, sob qualquer forma, no todo ou em parte, implicará em sanções cíveis e criminais cabíveis, incluindo a obrigação de reparação de todas as perdas e danos causados, nos termos da Lei nº 9.610/98 e de outras aplicáveis.