Resumo do Relatório

FX Dashboard: The US Dollar View and Its Implications for EM Currencies

(2 votes, average: 5,00 out of 5)

(2 votes, average: 5,00 out of 5)You need to be a registered member to rate this.

Since the end of the last year, the US dollar (DXY index) has persisted around its strongest level in almost two years. In doing so, the dollar has broadly followed my script; see Value of Euro as a Hedge for EM Currencies in Times Like These and Speculative Long Dollar Positions Highest Since 2019. I expected the dollar to remain strong by being at one of the two ends of the dollar smile, depending on which of the following scenarios played out:

- Rising US Treasury yields: As expectations of more aggressive monetary tightening by the Fed got priced in the curve, I expected rising interest rate differential to support the dollar. This should continue at least until the market becomes comfortable with the pricing of rate hikes in the curve.

- Risk Aversion: My concern was the potential of a correction in US equity markets if the Omicron wave results in weaker growth.

As it turned out the dollar has oscillated between the two ends of the smile:

- The US rates curve has gone from pricing in 1 rate hike in 2022 at the end of last year to 6 rate hikes now.

- The US equity market has suffered a correction on a combination of activity data turning weaker in Q1, imminent Fed tightening, and the risk of Russia invading Ukraine.

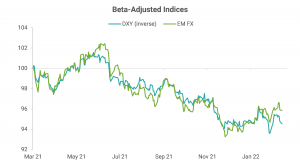

As a result, both the interest-rate differential and risk aversion have been supportive of the US dollar, which in turn has weighed on global currencies, particularly EM currencies as the chart below demonstrates.

Data Source: Refinitiv; Note: EM FX = equally weighted index of spot returns of 22 currencies

What should we expect for the dollar and EM currencies going forward?

- I don’t expect the dollar to depreciate meaningfully until:

- US rates volatility starts declining, as evidenced by the MOVE index which is at its highest since 2013 except for the brief spike in March 2020, and

- The risk of Russia invading Ukraine drops materially and Covid-related growth concerns dissipate to no longer weigh on US equities.

- In terms of timing, the dollar should remain strong at least until the March FOMC. The Fed could possibly provide guidance at the meeting with which the market is comfortable enough to allow for US rates volatility to drop. Also, by then, there should be more clarity on Russia’s intentions one way or another: either they would have invaded Ukraine already, but if not, then the likelihood of an invasion would drop sharply as Russia’s leverage – in the form of holding back the natural gas flow to the EU – in its negotiations with the West would weaken once the winter months end.

- Until then, the risk is for the dollar is to the upside, which in turn is likely to be a headwind for EM currencies:

- While the volatility of the US dollar has picked up, it is still below its long-term average (see the first chart below), indicating upside risks. The volatility of EM currencies is even lower.

- Long dollar positions have been reduced considerably in the past couple of weeks as the second chart below shows. The risk thus leans towards a build-up of these positions.

Data Source: Refinitiv; Note: EM FX = equally weighted index of spot returns of 22 currencies

- However, once we get past the risks discussed above by getting clarity on the Fed’s path and stability in US equities, then the dollar should depreciate as the year progresses, creating a favorable environment for EM currencies:

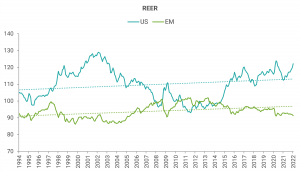

- In terms of valuations, the dollar is close to its most expensive since 2003, as demonstrated by the chart below showing real effective exchange rates. In contrast, EM currencies are at their cheapest since 2005.

- While the growth differential of the US with much of the rest of the world favored the US last year, the differential is due to narrow this year, particularly against other advanced economies, as per IMF forecasts.

Data Source: BIS

Best Longs / Best Shorts

- The list of underperformers based on my models in the attached FX Dashboard pdf remained unchanged with Israeli shekel (ILS) and the Philippine peso (PHP) on it.

- The list of outperformers also stayed unchanged with Peruvian sol (PEN), Polish zloty against the euro (EURPLN), Czech koruna against the euro (EURCZK), Hungarian forint against the euro (EURHUF), and Brazilian real (BRL) on it.

Best Crosses

- The list of the preferred relative-value trades based on my models expanded to Long RUB vs Short BRL or PEN or PLN and Long ILS vs Short BRL.

- The 3m expected returns for these pairs are in the range of 8-11% (not annualized), assuming mean reversion.

Gautam Jain

Estrategista - Ph.D, CFA

New York, EUA

Aviso legal

DISCLAIMER: Este Relatório de Análise foi elaborado e distribuído pelo Analista, signatário unicamente para uso do destinatário original, de acordo com todas as exigências previstas na Resolução CVM nº 20 de 26 de fevereiro de 2021 e tem como objetivo fornecer informações que possam auxiliar o investidor a tomar sua própria decisão de investimento, não constituindo qualquer tipo de oferta ou solicitação de compra e/ou venda de qualquer produto. As decisões de investimentos e estratégias financeiras devem ser realizadas pelo próprio leitor, os Analistas, ou a OHMRESEARCH não se responsabilizam por elas. Os produtos apresentados neste relatório podem não ser adequados para todos os tipos de investidores. Antes de qualquer decisão de investimentos, os investidores deverão realizar o processo de suitability no agente de distribuição de sua confiança e confirmar se os produtos apresentados são indicados para o seu perfil de investidor. A rentabilidade de produtos financeiros pode apresentar variações e seu preço ou valor pode aumentar ou diminuir num curto espaço de tempo. Os desempenhos anteriores não são necessariamente indicativos de resultados futuros. A rentabilidade divulgada não é líquida de impostos. As informações presentes neste material são baseadas em simulações e os resultados reais poderão ser significativamente diferentes.

O(s) signatário(s) deste relatório declara(m) que as recomendações refletem única e exclusivamente suas análises e opiniões pessoais, que foram produzidas de forma totalmente independente e que a OHMRESEARCH não tem qualquer gerência sobre este conteúdo. As opiniões aqui expressas estão sujeitas a modificações sem aviso prévio em decorrência de alterações nas condições de mercado. O Analista responsável pelo conteúdo deste relatório e pelo cumprimento da Resolução CVM nº 20/21 está indicado acima, sendo que, caso constem a indicação de mais um analista no relatório, o responsável será o primeiro analista credenciado a ser mencionado no relatório. Os analistas cadastrados na OHMRESEARCH estão obrigados ao cumprimento de todas as regras previstas no Código de Conduta da APIMEC para o Analista de Valores Mobiliários e no Manual de Controles Internos para Elaboração e Publicação de Relatórios da OHMRESEARCH. De acordo com o art. 21 da Resolução CVM nº 20/21 caso o Analista esteja em situação que possa afetar a imparcialidade do relatório ou que configure ou possa configurar conflito de interesse, este fato deverá estar explicitado no campo “Conflitos de Interesse” deste relatório.

O conteúdo deste relatório é de propriedade única do Analista signatário e não pode ser copiado, reproduzido ou distribuído, no todo ou em parte, a terceiros, sem prévia e expressa autorização deste Analista. Todas as informações utilizadas neste documento foram redigidas com base em informações públicas, de fontes consideradas fidedignas. Embora tenham sido tomadas todas as medidas razoáveis para assegurar que as informações aqui contidas não são incertas ou equívocas no momento de sua publicação, o Analista não responde pela veracidade das informações do conteúdo.

Para maiores informações, pode-se ler a Resolução CVM nº 20/21 e o Código de Conduta da APIMEC para o Analista de Valores Mobiliários. Este relatório é destinado exclusivamente ao assinante da OHMRESEARCH que o contratou. A sua reprodução ou distribuição não autorizada, sob qualquer forma, no todo ou em parte, implicará em sanções cíveis e criminais cabíveis, incluindo a obrigação de reparação de todas as perdas e danos causados, nos termos da Lei nº 9.610/98 e de outras aplicáveis.