Resumo do Relatório

FX Dashboard: South African Rand’s Outperformance is Overdone

(1 votes, average: 5,00 out of 5)

(1 votes, average: 5,00 out of 5)You need to be a registered member to rate this.

In an environment in which external drivers overwhelm, country-level macroeconomic developments typically take a backseat. As I discussed in Rates in Asia Underperform Following the Fed Hike and Russia’s Invasion, currently there are two such disruptive ongoing events: monetary tightening by the US Fed and Russia’s invasion of Ukraine.

Given the uncertain, yet powerful, implications of these events for the global economy, the market is understandably struggling to price the potential scenarios. It is difficult to read too much into the price action on a day-to-day basis, especially at a country level. Indeed, such an environment may be ripe with opportunities as short-term mispricing can occur.

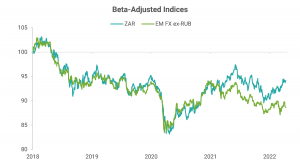

Data Source: Refinitiv; Note: EM FX = equally weighted index of spot returns of 21 currencies excluding Russian ruble

One instance of mispricing could be the South African rand (ZAR). Most factors, as I discuss below, do not justify its outperformance, especially on a year-to-date basis, as the chart above shows. Before going into those, even the two main factors that have been cited as the reasons justifying the strong performance of the currency on a relative basis are becoming less appealing. Specifically:

- High carry: The implied yield from 3-month ZAR forwards is currently 5.5%, which is not particularly high in an EM context as it matches the current average of 20 liquid emerging market currencies (excluding Turkish lira (TRY) and Russian ruble (RUB)). More importantly, instead of looking at the level of the nominal carry, I like to look at it in two different ways which I deem to be better indicators:

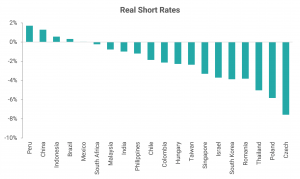

- Real carry: Since inflation is currently elevated in most emerging countries, it is better to look at the carry in real terms. When the 3-month implied yield is deflated with the current headline CPI (see below), the real carry for the rand is on the high side versus other EM currencies, but it is still negative.

Data Source: Refinitiv

-

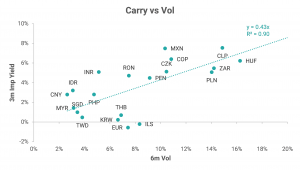

- Carry versus volatility: To judge whether the carry of currency is high on a risk-adjusted basis, I also look at the carry versus volatility chart (see below). On this chart, the rand does not look attractive.

Data Source: Refinitiv

- Current account surplus: High commodity prices have been beneficial for South Africa as it exports among others, platinum, coal, and iron ore. Indeed, the current account ran a surplus of 3.8% in 2021, which contrasts with the average annual deficit of around 2.5% during the previous decade. However, platinum and iron ore prices are off their 2021 peaks. Not surprisingly, Bloomberg consensus forecasts point to a sharp drop in the surplus in 2022, followed by a return of deficits in the coming years.

Over the coming months, the negative factors should start overwhelming, in my view:

- Growth remains an issue: The SARB raised its GDP growth forecast for 2022, which was one of the drivers behind the rand’s recent strong performance. However, it lifted its projection to a lethargic 2% from 1.7%. There are several reasons behind the cyclical and structural weakness of the South African economy:

- Covid continues to bite: Even in the context of the global poor response to Covid with few exceptions, South Africa’s management of the pandemic has been lacking. Two years into the pandemic, a paltry 36% of the population has received at least one shot. After four waves of coronavirus cases, with each peaking at a higher level than the previous, test positivity is rising again, although from a low level.

- Need for reforms: In his state-of-the-nation address, President Cyril Ramaphosa emphasized that the private sector should be the one leading job creation with support from the government. This is an attempt at a shift in the mindset since his party, the ruling African National Congress (ANC), has long been a proponent of a state-run economy. It is a steep hill to climb though as corruption runs high. As a recent example, for a top post, the ANC picked a former mayor, who has been charged with corruption and is a close ally of the disgraced former president Zuma. The areas that need urgent attention are:

- Unemployment: South Africa has favorable demographic dynamics with a growing and young population. However, workers suffer from a lack of opportunities, poor education and training, and low skill levels, which lead to low productivity. Unemployment is unsustainably high at above 35%.

- Electricity shortage: Power supply is a major growth impediment in South Africa. The electricity infrastructure has been degrading for years with rising frequency and duration of power outages.

- Monetary policy: The rand got a boost when the South Africa Reserve Bank (SARB) delivered a 25 bp rate hike in March, with 2 votes out of 5 for a 50 bp hike. The curve is pricing further rate hikes exceeding 200 bp in 1 year. SARB’s model is suggesting less with 150 bp of rates hikes in 2022, i.e., another 100 bp for the remainder of the year. Given the growth outlook for South Africa described earlier combined with the risk of a global recession due to the two events mentioned at the outset, my view is that the SARB would not hike as much as currently priced and possibly less than even the SARB model. Although the headline CPI is due to breach the upper end of the target band of 3-6% in the coming months, it should drop for the remainder of the year. SARB’s CPI forecast for Q4 is 5.4% YoY.

- Debt profile: Moody’s changed the outlook for the South African credit from negative to stable, which was treated as a positive catalyst for the rand even though it maintained the credit rating at two notches below investment grade. Although the fiscal balance has improved with support from high commodity prices, the debt remains at concerning levels with the Treasury expecting it to peak at 75% of GDP. Moreover, the continued state support needed for parastatals indicates that the risk is to the upside. Eskom, for example, is likely to need more state support due to rising oil prices.

- Valuation: EM currencies on average are around 3% cheap in real effective exchange rates (REER) terms when comparing the current REER levels with its 10-year average. The rand, however, is expensive in this measure by around 2%. In valuation terms, therefore, it is not as attractive as other EM currencies, particularly in Latin America (see Latin American Currencies on Top).

To conclude, while the global environment remains quite unpredictable in the near term, I would look for opportunities to short the rand since most of the positive catalysts for the currency are now behind and it should narrow the gap with the broad EM FX universe (see the chart below).

Data Source: Refinitiv; Note: EM FX = equally weighted index of spot returns of 21 currencies excluding Russian ruble

Best Longs / Best Shorts

- To the list of underperformers based purely on my models in the attached FX Dashboard pdf, I added Hungarian forint against the euro (EURHUF) as its z-score rose above 1.

- The list already had Israeli shekel (ILS) and Taiwan dollar (TWD) on it.

- From the list of outperformers, I removed Chilean peso (CLP) as its z-score receded.

- The list now consists of Peruvian sol (PEN), Brazilian real (BRL), Colombian peso (COP), and South African rand (ZAR).

Best Crosses

- The list of the preferred relative-value trades based purely on my models changed to Short BRL vs Long Hungarian forint (HUF) or Polish zloty (PLN) or Czech koruna (CZK) or TWD or Romanian leu (RON).

- The 3m expected returns for these pairs are in the high range of 22-25% (not annualized), assuming mean reversion.

Gautam Jain

Estrategista - Ph.D, CFA

New York, EUA

Aviso legal

DISCLAIMER: Este Relatório de Análise foi elaborado e distribuído pelo Analista, signatário unicamente para uso do destinatário original, de acordo com todas as exigências previstas na Resolução CVM nº 20 de 26 de fevereiro de 2021 e tem como objetivo fornecer informações que possam auxiliar o investidor a tomar sua própria decisão de investimento, não constituindo qualquer tipo de oferta ou solicitação de compra e/ou venda de qualquer produto. As decisões de investimentos e estratégias financeiras devem ser realizadas pelo próprio leitor, os Analistas, ou a OHMRESEARCH não se responsabilizam por elas. Os produtos apresentados neste relatório podem não ser adequados para todos os tipos de investidores. Antes de qualquer decisão de investimentos, os investidores deverão realizar o processo de suitability no agente de distribuição de sua confiança e confirmar se os produtos apresentados são indicados para o seu perfil de investidor. A rentabilidade de produtos financeiros pode apresentar variações e seu preço ou valor pode aumentar ou diminuir num curto espaço de tempo. Os desempenhos anteriores não são necessariamente indicativos de resultados futuros. A rentabilidade divulgada não é líquida de impostos. As informações presentes neste material são baseadas em simulações e os resultados reais poderão ser significativamente diferentes.

O(s) signatário(s) deste relatório declara(m) que as recomendações refletem única e exclusivamente suas análises e opiniões pessoais, que foram produzidas de forma totalmente independente e que a OHMRESEARCH não tem qualquer gerência sobre este conteúdo. As opiniões aqui expressas estão sujeitas a modificações sem aviso prévio em decorrência de alterações nas condições de mercado. O Analista responsável pelo conteúdo deste relatório e pelo cumprimento da Resolução CVM nº 20/21 está indicado acima, sendo que, caso constem a indicação de mais um analista no relatório, o responsável será o primeiro analista credenciado a ser mencionado no relatório. Os analistas cadastrados na OHMRESEARCH estão obrigados ao cumprimento de todas as regras previstas no Código de Conduta da APIMEC para o Analista de Valores Mobiliários e no Manual de Controles Internos para Elaboração e Publicação de Relatórios da OHMRESEARCH. De acordo com o art. 21 da Resolução CVM nº 20/21 caso o Analista esteja em situação que possa afetar a imparcialidade do relatório ou que configure ou possa configurar conflito de interesse, este fato deverá estar explicitado no campo “Conflitos de Interesse” deste relatório.

O conteúdo deste relatório é de propriedade única do Analista signatário e não pode ser copiado, reproduzido ou distribuído, no todo ou em parte, a terceiros, sem prévia e expressa autorização deste Analista. Todas as informações utilizadas neste documento foram redigidas com base em informações públicas, de fontes consideradas fidedignas. Embora tenham sido tomadas todas as medidas razoáveis para assegurar que as informações aqui contidas não são incertas ou equívocas no momento de sua publicação, o Analista não responde pela veracidade das informações do conteúdo.

Para maiores informações, pode-se ler a Resolução CVM nº 20/21 e o Código de Conduta da APIMEC para o Analista de Valores Mobiliários. Este relatório é destinado exclusivamente ao assinante da OHMRESEARCH que o contratou. A sua reprodução ou distribuição não autorizada, sob qualquer forma, no todo ou em parte, implicará em sanções cíveis e criminais cabíveis, incluindo a obrigação de reparação de todas as perdas e danos causados, nos termos da Lei nº 9.610/98 e de outras aplicáveis.