As per the request of some of our contacts, bellow you will find the English version of the article written by Roberto Dumas, Daniel Passos Miraglia and me about the cost of opportunity and asset bubble dynamics published in the site of @omninvest and also in the platform of @APIMEC (Brazilian Analyst Association).

In moments of crisis and isolation like the present, we tend to think about human nature, and – why not? – that of investors, and analysts.

Every age, every situation, has its pathological pessimists, incorrigible optimists – and realists. But in times of crisis like the present – likely to be the worst in a century for global growth with the exception of two world wars – we see the emergence of one more, somewhat anomalous, market personality: the hyper-optimistic “cheerleader”.

We have nothing against optimism ! We have nothing in principle against always betting positively on the future of asset prices – but we do think the mask we are currently forced to use to cover our nostrils and mouth should not be extended to cover our eyes…

We have written many books, about how history repeats itself in times of financial meltdown. We found that after an asset bubble burst (example: earlier this year), the monetary authorities usually make the same mistake of planting the seeds of the next bubble – which will in turn burst, with further heavy burdens on the real economy.

Faced with evidence of previous crises, however, economic and financial agents come up with the same cry:

“This time is different”.

No matter how similar crises appear to be, there will always be someone sufficiently intelligent and apparently lucid to explain that the recent boom is the result of: technological innovations (for the 2000 dot-com bubble); or … financial innovations (derivatives, securitization and HBJB sub-prime collapse of 2008) – and they will make little or nothing of what could have been learned from previous disasters.

(For the logic, see: Roubini (2010), Reinhart and Rogoff (2009)[1], and Dumas (2016)[2].)

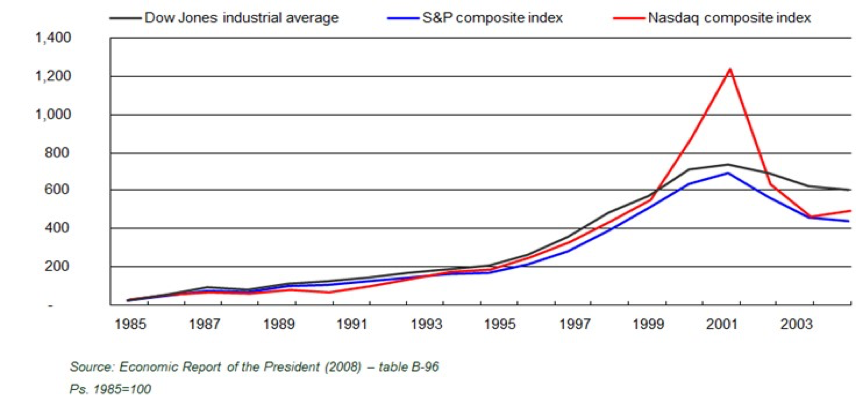

Who doesn’t remember the Internet boom – and its stellar rise of the Nasdaq?

When that was happening, analysts found they were unable to apply any accepted valuation method to justify the massive rise in stock prices. From 1995 to 2000 the Dow Jones index rose 139%; the S&P composite rose 63%; – and the Nasdaq rose no less than 309%. Here’s how it looked:

What did Wall Street mandarins say?

“The manner of pricing companies has evolved.”

As every stock analyst knows, the most commonly used methods of pricing shares are: (i) discounting projected cash flows to present value (DCF); and (ii) comparison of multiples (Price/Book, EV/Ebitda, etc.)

So how were analysts going to justify that scandalous increase in prices of Internet-sector stocks if no valuation method explained it?

However peculiar it may seem, investment banks and research houses were taken over by a perception of – perhaps we should call it? – ‘inversion of causality’.

If no known method could justify the market’s actual pricing – since very few of these companies were expected to generate profit (and much less, cash flow) in the next five or 10 years – then, they said, let a new method be adopted. And they resorted to a multiple, EV/Sales, the use of which was, in a proper analysis, completely unjustifiable in the context – indeed, intellectually scandalous!

With this new … talismanic method of pricing companies, it was just about possible to ‘justify’ the rise in the Nasdaq. The scale of the ‘inversion of causality’ was alarming. Instead of the analyst pricing companies that were the subject of his analysis using long-accepted methods to justify a buy, or otherwise, for a given share, everyone moved to a new method that merely supported, illustrated, the rise in stock prices that was happening.

Look at this from the point of view of a practical fund manager at the time: who would be insane enough to confront a wave of pleasurable euphoria by stating loud and clear that these price rises were unjustified – that in the final analysis they were only the result of irrationality by economic agents?

No-one wanted to do that. So they looked for a new methodology of pricing, which would give technical support to the price rise that was happening. They would say: “The old pricing methodologies no longer apply to a scenario of technological evolution like this one”.

One could even say, with considerable support from experience, that a large part of the players in this market were aware of the irrationality of that upward movement in stock prices. But how could they not take advantage – how not to surf on that wave?

How could they allocate clients’ funds in government bonds with minimal return, if a new wave of stock price rises could make clients happier? Certainly it would have been a losing gambit in any attempt by funds – already competing bitterly – to attract new clients.

Should the fund manager contain himself, stick to the intellectual straight-and-narrow, losing all his clients rapidly to a manager who continued to surf the wave of rising prices –even though there was no technical support for the phenomenon?

Even if he did, he would soon be taken to task, and probably fired, by his manager – or kicked out of the market altogether. Why hold on to a fund manager who routinely produces returns which (in the short term) are not even 10% of those achieved by most of his peers?

Note the risk that even the most qualified administrator, analyst and/or manager runs, here, of simply becoming intellectually corrupted – placing a large majority of his clients’ funds in assets which are rising in price to levels that have no support in any honest analysis on fundamentals.

Resisting waves like this is not easy, but by ‘surfing’ them, investors are only causing their prophecies to self-fulfil (in the short term) by fanning a wave of euphoric, pleasurable, sentiment.

It has been said that: the worst thing for a manager is to be inside a bubble when it bursts, and the second worst thing is not to be inside it, while it is forming.

In a bubble, if the expectations of financial and economic agents suffer any change of mood, however small – even if the protagonist is in another nation – this can lead to a mass herd-stampede for the exit.

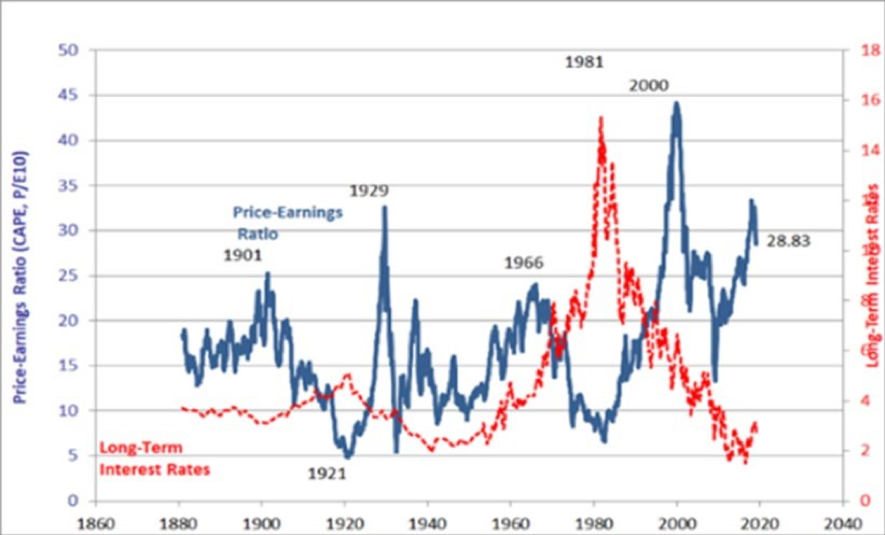

We published several articles in journals in 2019 alerting to excess optimism on the performance of the S&P 500, which according to Robert Shiller’s CAPE ratio chart (below) has never been so high – except in 1929, and 2000 – and their comparison with the forecasts for the global economy. The story is: from euphoria … to depression; from excess of exorbitant optimism, to an excess of high pessimism.

This time, it does not seem, to us, to “be different”.

This present essay at no time seeks to convince any investor not to surf on a pleasurable wave, such as some say may be forming on stock exchanges’ horizons, generated by the monetary easing (QE) provided by the US Federal Reserve, the European Central Bank and the Bank of Japan. But it becomes imperative that the professional investor, and also beginners, should have fully in mind the risk they are running.

In Brazil, one of the main arguments for investors’ attraction to stocks amid the pandemic is that the basic (Selic) interest rate is extremely low, so that it’s time, once again, to run risks – as if the pandemic has not influenced, or will not influence, the cash flows of various listed companies.

Before we go on to technical proofs, to those who say that the present level of the Selic (2.25% p.a. on June 18th , 2020) indicates the demise of fixed income, and that this obliges people to move into stocks, it’s not a bad idea to remember the case of Japan, precursor of what the world is going through today.

Up to the time of publication of this paper, the Japanese fixed income market had not disappeared in a puff of smoke, and the Nikkei index was not in the stratosphere – on the contrary, it was 40% below its peak of exactly 30 years ago, which was when interest rates fell to zero in Japan.

Standard theory tells us that in applying DCF (discounted cash flow), the interest rate that is appropriate as proxy for opportunity cost is the one determined by ke or WACC. This paper does not aim to demonstrate these methods. What we focus on is the major fallacy – perhaps opportunistic – of many advisers when they point to the basic Selic rate (in Brazil) as part of opportunity cost: the risk-free rate.

Consider: investment in shares requires a long-term view. When projecting the cash flow of a given company, it is clearly essential to adopt a risk-free rate for the long term, not a short-term one. That is to say: the risk-free rate that should be part of the opportunity cost of the stockholder (or the company) is the rate found at the long point of the risk-free rate curve, which certainly is not the Selic rate (currently 2.25% p.a.).

To make things even more complicated, even a long-term Brazilian interest rate cannot be used on its own, because the ‘risk-free’ label does not match very well with the Brazilian economy. What is used is the geometric mean (over 10 or 20 years) of the 10-year yield on US federal securities, converted into Reais (BRL). Then one has to add Brazil risk (as measured by EMBI), and the so-called market risk premium (geometric annual return of the S&P 500 from 2008 to 2019, less the return on 10-year US Treasuries in that period), multiplied by the beta (b) of the corresponding company, and adding, further, the inflation differential between Brazil and the US (so as to bring the return required by the stockholder into the local currency – in this case, the Real). OK. That’s it. Now we have our ke (cost of equity).

Thus, the discount rate to be used as a stockholder’s opportunity cost for pricing Brazilian companies has been dramatically underestimated.

The difference – or should we call it the intellectual dishonesty – in this respect, is scandalous.

An adviser who uses the Selic rate as a proxy for the risk-free rate to build the stockholder’s return is simply making a crass error. As we all know, a lower discount rate (with all else constant) simply inflates the present value of future cash flow – justifying higher prices. Now, think of the Internet bubble.

Another aspect that has attracted a lot of attention in analyzing future cash flow is the ‘perpetuity’ commonly used in DCF.

It’s argued that the lower the interest rate, the better the country’s outlook. Here, note the difference between our optimism-addicted ‘cheerleader’, rousing his team from the edge of the field, glutted on wishful thinking – and the responsible adviser.

By opening up the narratives of these advisers, we can counter that the Selic (base) interest rate is at 2.25% not because we expect happy moments for the real economy ahead, but because, as a rule of thumb, the nominal interest rate of a country (one that is not subject to financial repression, such as China) should be equal to the expectation for nominal GDP growth.

We may express GDP as the sum of ‘income’ from the following components: wages (income from work), interest (income from capital), rentals (income from physical installations), and profit (income from the production process) – a simple formula:

GDP = wages (income from labor) + interest (income from capital) + rentals (income from physical facilities) + profit (income from the production process) + taxes (income of the government)

Looking from this point of view, the rule of thumb helps us to understand that the nominal growth rates that give rise to these flows of remuneration should be the same for all these factors, assuming that there is not a concentration of income in any one of these participants.

If, even so, the Central Bank continues its expansionist monetary policy by cutting interest rates, it’s because Brazil is tending not to grow more in the future, but to grow less, thus negatively affecting the cash flow of companies that the analyst is valuing. That is to say, in the method they apply and the way they apply it, some advisers get both the numerator and the denominator wrong.

Worse still, they – so lightly – assume that the only investment options are in Brazil, as if there were no alternative in the rest of the world: a local version of ‘TINA’: “There is no alternative”.

It happens that there are, yes, alternatives, and that diversification of currencies is something that is fundamental in finance theory, and very little applied in Brazil. Hold more than one currency! Always!

This is really a simple question of consistency.

Every investor has the liberty to use whatever discount rate or opportunity cost they wish. But if they want to use the Selic rate – of 2.25% – as a component of their discount rate, they should use the same 2.25% for GDP growth (nominal, not real), both in the projected years of the cash flow, and also in the perpetuity. I think we can say with a high degree of certainty that with these estimates of long-term GDP growth, we would have much lower profits in the average of companies than the market expects today.

So this kind of calculation is a case of: “You can’t have your cake and eat it too”!

Please note, again, that at no time in this paper are we asking an investor – whether professional or individual – not to surf a supposed wave, in this case enjoying the fruits provided by generous monetary stimuli. One might think: “As long as you’re catching fish, it doesn’t matter whether you’re using real or artificial bait.”

But we do feel obliged to alert investors who are witnessing this rise – especially individual investors – about the risk they are running.

It’s the job of an investment adviser to explain precisely the risk that the client is running, even if the justification is only that “there’s too much money in the market” and that, this being so, the investor should not miss this (supposed) opportunity.

However, we firmly believe that trying to ‘hide’ behind fallacious analyses that seek to provide a reason for a rise in stock prices is in our view inappropriate, and could lead people to run risks that are not within their suitability profile.

We know there is a clear sentiment that advisers and analysts should stay closer to the consensus. This is even expressed in the dictum: “I prefer to get it wrong with everyone than to get it right on my own”. But we have witnessed a wide range of advisers using weak, imprecise, and sometimes totally incorrect arguments, only to provide a fantasy-led support for their bias. This in itself can become the biggest risk in the market, causing inexperienced investors to misunderstand exactly what risks they are taking on.

Surf the wave, enjoy it, but understand the risks. And in the words of the legendary investor John Templeton:

“The four most dangerous words in the world of investing are: “This time it’s different”.

Roberto Dumas Damas

More than 30 years’ experience in Brazilian and international financial markets. Master’s degree in Economics from the University of Birmingham (UK); Master’s degree in Chines Economy from Fudan University (China); tutor and lecturer at Insper, Ibmec São Paulo, and the FIA Management Foundation of São Paulo, Brazil.

Daniel Passos Miraglia

30 years working in financial markets; USP award for excellence in Economics; Master’s degree in Finance with double certification (BSP, EOI Foundation of Spain).

Roberto Attuch Jr.

25 years in Latin American equities (Credit Suisse, Barclays). Currently, CEO/founder of OHMRESEARCH. Master’s degree in Risk Management from NYU; Diploma in Corporate Governance from Insead.

[1] Roubini, N. and Mihm, S. (2008): “Crisis Economics. A Crash Course in the Future of Finance”. Ed. Penguin Press NY Reinhart, C. and Rogoff, K. (2009): “This Time is Different. Eight Centuries of Financial Folly”. Ed. Princeton University Press

[2] Dumas, D., R. (2016): “Crises Econômicas Internacionais” – Ed. Saraiva

Gostou do texto?

Então cadastre-se gratuitamente para receber em seu e-mail nossas novidades e ofertas exclusivas.